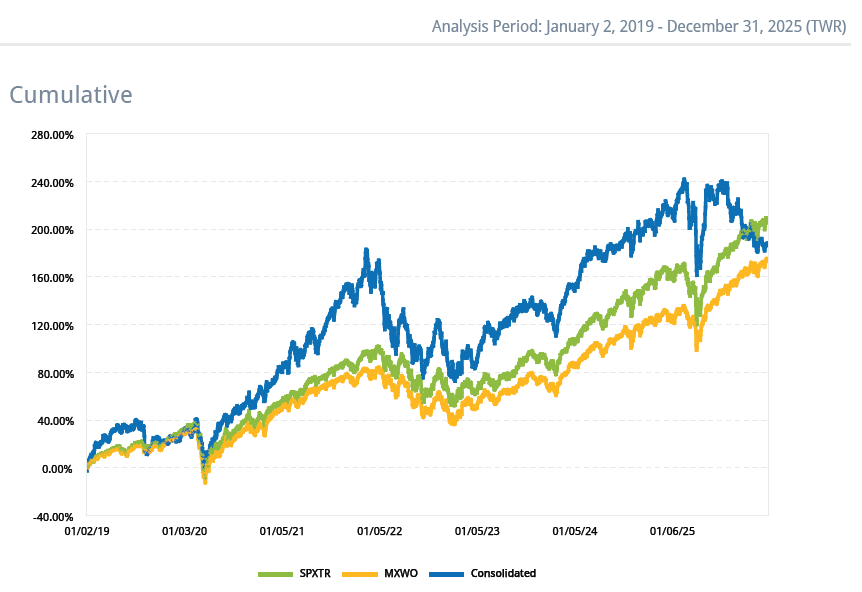

Historical performance (in €)

2019: +30.2%

2020: +41.8%

2021: +47.4%

2022: -29.9%

2023: +36.2%

2024: +24.3%

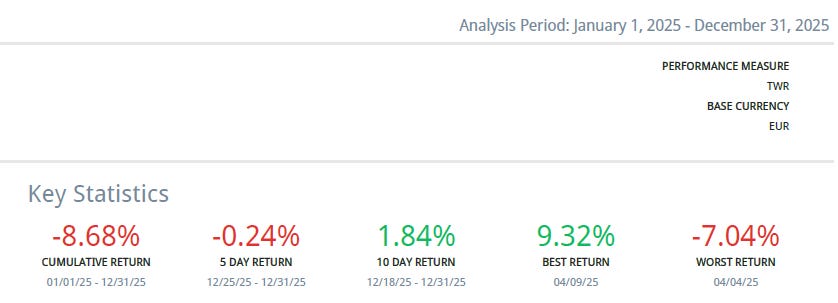

2025: -8.7%

CAGR 2019 - 2025 (7Y)

Portfolio: +16.7 %

S&P 500: +17.3%

MSCI ACWI: +14.3%

My portfolio closed 2025 with a return of -8.7%. At least since I’ve been keeping detailed records, it was the year with the largest divergence between my portfolio’s performance and the benchmark indices. It’s an uncomfortable gap, and I won’t pretend otherwise. Not so much because of the opportunity cost—had I simply indexed, the outcome would have been better and far less mentally taxing—but because watching family wealth decline is, in itself, psychologically difficult.

That said, the way I construct the portfolio (more than the specific company selection) is not designed to track the market, and this approach comes with both advantages and drawbacks. 2025 was a clear illustration of that trade-off. Early in the year, I increased my exposure to VMS, an industry that exhibits many of the characteristics I value most when investing. In hindsight, the timing could hardly have been worse. Even now, in 2026, the market continues to debate the terminal value of the industry. To increase that concentration, I chose to exit other positions that have since performed significantly better. In the short term, no one truly knows anything, and I know even less. I think it’s important to challenge the idea that a highly concentrated portfolio is a prerequisite for outperforming the market. Ultimately, what matters is being right and, just as importantly, making few mistakes. High concentration can become counterproductive if volatility pushes you into unforced errors—poor decisions made at precisely the wrong moments. Managing savings in your twenties is not the same as managing family wealth or the legacy you hope to leave your children. The responsibility is greater, and emotional control becomes a decisive factor in capturing those extra basis points one hopes to extract relative to the indices. That’s not something you learn by analyzing companies, reading investment books, or studying the biographies of great investors. It’s something you only truly learn by living through it.

This is not meant to be an emotional reckoning. Negative returns are an inherent part of this process, and while they’re never easy to accept, they tend to be highly instructive. Bad years create the space to revisit and question what you thought you understood. To calmly review each decision, identify mistakes, and improve in a game that ultimately rewards those who manage to survive, while resisting the temptation to take shortcuts along the way.

I trust my investment philosophy. Given my understanding of investing, it is the one that makes the most sense to me and, above all, the one that allows me to sleep best at night. While many investors focus primarily on just returns, I increasingly value return on time invested and peace of mind. That said, I do need to be more rigorous in the selection of businesses. I believe I’ve been guilty of overestimating the strength of the competitive advantages of several companies that, at the time, appeared very attractive. And this isn’t limited to investments that lost money; in hindsight, I’ve also misjudged businesses that ended up being profitable. What I’ve learned is that virtually all businesses possess some form of competitive advantage (otherwise, they wouldn’t exist in their current form) but not all advantages are created equal. Deciding where not to invest is just as important as deciding where to allocate capital. Expanding one’s circle of competence doesn’t necessarily mean expanding the list of investable companies. A broad circle of competence is valuable because the more you learn about different business models, the more aware you become of how little you truly know. That awareness of ignorance has made me more cautious and selective. Today, I genuinely believe there are only a handful of truly exceptional companies worldwide that deserve my attention, my time, and my capital. The standards I apply when selecting businesses continue to rise, and while this won’t eliminate mistakes, it should improve the success rate over time.

Beyond investing, 2025 was also a challenging year for our family in other—and far more important—ways. Life is rarely linear; it’s full of unexpected challenges that make periods of calm and routine especially meaningful. Fortunately, we are all healthy and united, and I’m optimistic that 2026 will be a good year for us.

Regardless of monetization, the blog remains an extremely valuable tool for reinforcing discipline and for continuing to learn about businesses I might not otherwise dedicate hours of focused study to. The barriers to entry for starting a blog are virtually nonexistent, and while the barriers to sustained success are higher, there is no shortage of capable voices around the world doing excellent work. For that reason, I want to sincerely thank everyone who chooses to support this small and modest project, fully aware that many alternatives exist. I can’t increase the posting frequency as much as I would if I could dedicate myself exclusively to the blog (my main occupation lies elsewhere) but if there is anything I can do to add more value, I would genuinely appreciate your feedback. Any suggestion that helps improve the quality of my work is welcome.

I don’t know how my portfolio will perform in 2026. What I do know is that I will continue to make gradual adjustments so that the lessons learned are reflected in its composition. In fact, I’ve already begun implementing some changes, which I’ll explain in greater detail in future posts. Finally, I want to thank both the paid subscribers who make this blog sustainable and all those who follow it closely.

Portfolio Update